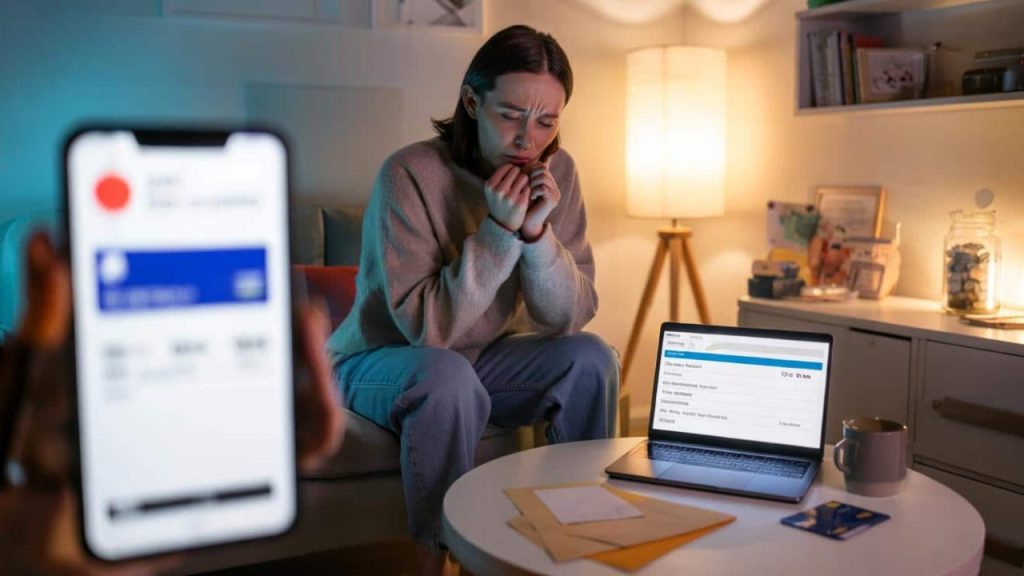

The notification sound from Marcus’s banking app made his stomach drop. At 67, the retired electrician had finally gotten comfortable with his monthly budget after years of careful planning. Then his water heater decided to flood his basement on a Tuesday morning, and suddenly he was staring at a $4,800 repair bill that wasn’t in anyone’s financial playbook.

“I felt like all those years of saving and planning just got wiped out in one morning,” Marcus later told his daughter. “It wasn’t just the money—it was wondering what else could go wrong.”

Marcus isn’t alone in this feeling. Unplanned expenses have a way of shaking our financial confidence to its core, creating ripple effects that go far beyond the immediate cost.

When Life Throws Financial Curveballs

Unplanned expenses don’t just drain bank accounts—they fundamentally change how we view our financial security. Whether it’s a medical emergency, car breakdown, or home repair, these surprise costs can derail even the most carefully crafted financial plans.

The psychological impact often outweighs the actual dollar amount. When we’re forced to dip into savings or take on debt for unexpected costs, it can trigger a cascade of worry about future financial stability.

The emotional toll of unplanned expenses often creates more lasting damage than the expense itself. People start questioning whether they’ll ever feel financially secure.

— Dr. Jennifer Walsh, Financial Psychology Researcher

Research shows that even middle-income households can see their long-term financial confidence plummet after a single major unexpected expense. The fear becomes less about the current situation and more about what might happen next.

The Real Numbers Behind Financial Surprises

Understanding the scope of unplanned expenses helps put the challenge in perspective. Here’s what American households typically face:

| Type of Emergency | Average Cost | Frequency |

|---|---|---|

| Medical Emergency | $1,200-$5,000 | 40% of adults annually |

| Car Repair/Replacement | $500-$3,500 | 65% of car owners annually |

| Home Maintenance | $800-$4,000 | 55% of homeowners annually |

| Job Loss Income Gap | $2,000-$8,000 | 15% of workers annually |

| Pet Emergency | $300-$2,500 | 30% of pet owners annually |

The most damaging aspect isn’t necessarily the size of these expenses, but how they cluster. Families often report that unplanned costs seem to come in waves—the car breaks down the same month the roof starts leaking.

Key factors that amplify the impact include:

- Limited emergency fund coverage

- Existing debt obligations

- Fixed income constraints

- Multiple dependents

- Seasonal income fluctuations

Most people can handle one unexpected expense, but it’s the second and third ones that really shake their confidence in their financial planning.

— Robert Chen, Certified Financial Planner

How Financial Confidence Takes the Hit

The relationship between unplanned expenses and long-term financial confidence operates on multiple levels. When people are forced to make emergency financial decisions, it often reveals gaps in their financial preparedness they hadn’t considered.

Many discover their emergency funds aren’t as robust as they thought. Others realize their insurance coverage has significant gaps. Some find themselves using high-interest credit options they swore they’d never touch.

The confidence erosion typically follows a pattern:

This cycle can persist long after the original expense is resolved. People who experience major unplanned costs often report feeling “gun-shy” about financial commitments for months or even years afterward.

I see clients who had one major unexpected expense three years ago, and they’re still afraid to spend money on anything beyond absolute necessities. The fear becomes paralyzing.

— Lisa Rodriguez, Financial Counselor

The Ripple Effects on Future Planning

Unplanned expenses don’t just affect current finances—they reshape how people approach future financial decisions. Many become overly cautious, potentially missing opportunities for growth or improvement in their financial situation.

Common long-term behavioral changes include:

- Over-saving in low-yield accounts

- Delaying necessary purchases or upgrades

- Becoming overly focused on worst-case scenarios

- Abandoning long-term financial goals

The irony is that while people think they’re protecting themselves, these overly conservative approaches can actually harm their long-term financial health. Money sitting in savings accounts earning minimal interest loses purchasing power over time.

Some families also develop what financial counselors call “expense anxiety”—constantly worrying about what might go wrong next. This mental state can be exhausting and often leads to poor financial decision-making driven by fear rather than logic.

The goal isn’t to eliminate all financial risk—that’s impossible. It’s about building systems that can absorb shocks without derailing your entire financial life.

— Mark Thompson, Financial Resilience Expert

Building Back Financial Confidence

Recovery from the confidence-shaking effects of unplanned expenses requires both practical and emotional work. The practical side involves strengthening financial defenses, while the emotional side focuses on rebuilding trust in your financial planning abilities.

Effective strategies include creating more robust emergency funds, reviewing insurance coverage, and developing multiple backup plans for common scenarios. But equally important is reframing how you think about unexpected expenses.

Rather than viewing them as financial failures, successful recovery often involves accepting that unplanned expenses are a normal part of life. The goal becomes building financial resilience rather than trying to prevent every possible expense.

Many people find it helpful to track their recovery progress and celebrate small wins. Rebuilding an emergency fund or successfully handling a smaller unexpected expense can help restore confidence gradually.

FAQs

How much should I save for unplanned expenses?

Most financial experts recommend 3-6 months of living expenses, but start with $1,000 and build from there.

Should I use credit cards for emergency expenses?

Only as a last resort, and have a clear payoff plan before using them.

How do I know if my emergency fund is adequate?

Review your last year’s unexpected expenses and ensure your fund could cover similar situations.

Can insurance help reduce unplanned expense impact?

Yes, proper health, auto, and home insurance can significantly reduce your out-of-pocket costs.

How long does it take to rebuild financial confidence?

It varies, but most people report feeling more secure within 6-12 months of implementing stronger financial defenses.

Should I sacrifice long-term goals to build emergency savings?

Balance is key—maintain some long-term investing while building your emergency fund gradually.